By | Shafeek Seddiq

By now many of you who have been financially impacted by the COVID-19 have applied or are in queue to apply for . Applicants who were approved during the initial round will be receiving their loans proceeds soon. Others should prepare and be ready for the next round.

After you spend the funds you received from the PPP, then what? It is one thing to get the loan, another to make sure you qualify for loan forgiveness. Once you receive your loan funds, your 8-week loan forgiveness period begins. Thus, it is very important to understand what to spend the money on and what documents to keep because non-compliance will require you to pay back the loan or part of it. Once this 8-week period ends, you will need to submit these documents to the lender to audit. The goal is to make sure your loan is forgiven.

Understanding the Purpose of the Payroll Protection Plan

Understanding the purpose of the loan is important because it will inform and guide you on what to spend your loan money on and how to keep records.

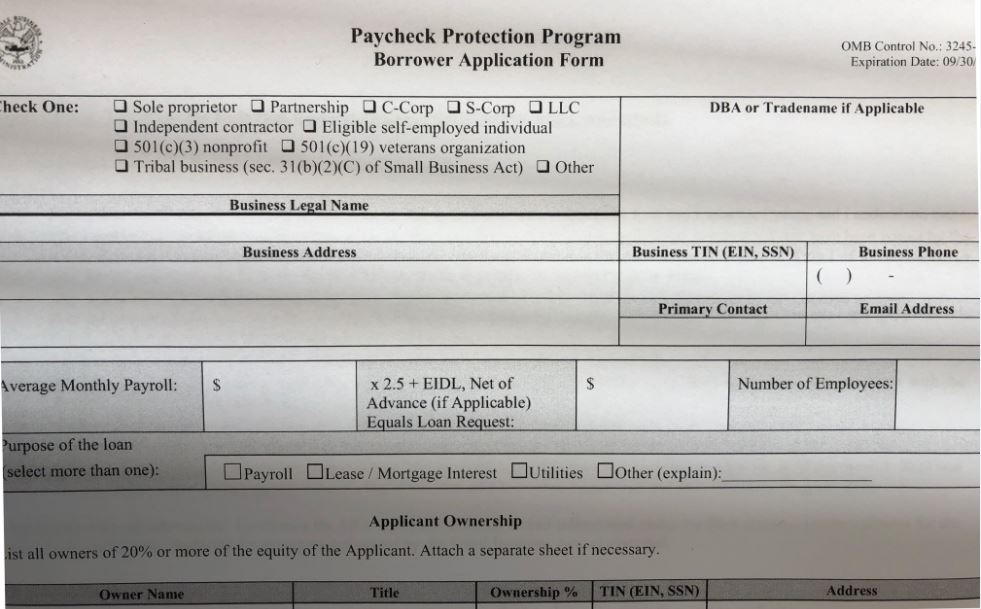

The purpose of the PPP loan is to protect the paycheck and that’s what it should be used for – to pay employees. It also explains what is included in payroll and how to calculate, and to include mortgage, rent, utilities and benefits.

Let’s assume you own a small business (restaurant, grocery store, dental office, beauty salon, and the likes) that has been directly impacted by the COVID-19, and you have:

- Employees including yourself: 5

- Your average monthly payroll: $10,000 ($120,000 total annual payroll for five employees divided by 12 months).

- Calculate your annual total payroll cost for all five employees.

- Payroll cost include:

- salary, wages, commission, or tips capped at $100,000 per year for each employee;

- employee benefits;

- state and local taxes assessed on compensation;and

- for independent contractor or sole proprietor wages , commission, income or

- Other expenses: Mortgage interest, rent and utilities: $5,000 per month

- Add Payroll and Other expenses, multiply by 25% = $18,750 (($10,000 + $5,000)X25%)

It depends on the date you receive the money in your bank account, you should start setting up your records in accordance with the purpose and the above outline.

Factors Considered in Forgiving the Loan

Keep in mind the following factors when you start spending the money:

- Eight Weeks: The eligible expenses are the ones incurred during this period.

- Percent Spending on Payroll Rule: You must spend at least 75% of your loan on payroll. Note calculation and outline above as to what payroll means.

- Seventy-Five Percent Pay Rule: You must pay at least 75% of the total salary to your employees and yourself.

- Rehire Until June 30, 2020: You can rehire your staff that you let go but payment was decreased by more than 25%.

- Maintain Staffing: You must maintain certain numbers of employees on your payroll or you risk not being qualified for forgiveness or forgivable expenses will be reduced proportionately.

Recordkeeping During the 8-Week Spending Period

Recordkeeping and documents of the 8-week spending period are required to be submitted with your forgiveness application and will likely result in that loan forgiven. Please ask your lender before you start spending money on what additional documents or records are required to maintain or submit as part of the PPP forgiveness application. But, at a minimum, keep documents for the following expenses:

- Number of full-time employees on payroll;

- Pay rate, taxes, retirement, and other benefits; and

- Mortgage interest, rent, and utilities payments (canceled checks, payment receipts, bank account statements).

When to Apply for Loan Forgiveness

Your lender will provide you application and instructions on where to apply. Once completed, your lender will process your application along with the documents you are keeping during the eight weeks.

The law requires your lender to provide you with a response within 60 days of the application.

In the event you are not approved for forgiveness, work with your lender and provide additional documentation so that your application may be reevaluated. Otherwise, your loan is deferred for the first six months and thereafter will continue to accrue interest at 1% for the remainder of the 2-year period. But you can pay your loan any time, as there is no prepayment penalty.

Remember that the CARES Act and the PPP are unprecedented, and the Small Business Administration is still working to figure out how all of this works and what everything means. The SBA is continually updating its guidance, so be on the look-out for such information. Work with the lender or lawyer or accountant to keep you abreast of any new developments, allowing you to be better prepared for achieving that goal: getting your loan forgiveness.

If you have questions about this article, please feel free to contact me at: shafeek@seddiqlawfirm.com or 703-558-9311 or through Facebook at https://www.facebook.com/SeddiqLaw/?modal=admin_todo_tour